Report on retail sales of wiring. Template for analyzing sales and profits in a company. Trade and reflection of retail revenue in NTT

Reflection in the 1C retail program is possible in two ways:

- Trade at points of sale without automation (NTT);

- Trade at points of sale with automation and cashless payment options.

In the first case, the system does not assume the presence of an online connection with the database. In this case, the point of sale exists autonomously, for example, it is a kiosk or an open tray installed on the street.

In the second case, standard trading is carried out, but using retail prices and creating a “Report on retail sales».

Trading and recording revenue in NTT

When keeping records trading activities For non-automated points of sale, the following procedure is assumed:

- Moving goods to the point of sale;

- Carrying out inventory;

- Fixation of revenue with a cash receipt order;

- Generating a sales report based on inventory.

Taking into account the fact that in this case exclusively retail revenue is considered, you will need to consider such documents as: “Cash receipt order” and “Retail sales report”.

In the process of conducting manual trading, there are no requirements for daily reflection of data on revenue and product sales volumes. The period for entering information and conducting inventory is determined by the selling company independently.

It should be noted that in this case, the primary cash order is the cash receipt order, and only after that the work on preparing the sales report is carried out. It is advisable to consider a specific example:

Creates a PKO for the “Retail Revenue” operation. The non-automated NTT point acts as a warehouse.

After creating the document, we observe the created transactions.

It is noticeable that for account 90.01.1 there is no third subaccount. Moreover, it cannot appear, since the document does not contain data on sales volume.

Next, a report on retail sales is created, and the system will independently enter the required type of transaction. Let's assume that an inventory has already been carried out and a corresponding report has been created based on its data.

We post the document and monitor the created postings

It is not difficult to notice the reversal of the posting created by PKO and filling in the data of the third subaccount in the postings. The implementation of this mechanism is required for the correct reflection of data at the end of the reporting period.

Trading at automated points of sale

When using automatic points of sale, it is possible to reflect revenue through the “Retail Sales Report”. In this case, the order in which actions are performed requires the opposite list of actions.

First, a sales report is generated. Select " Retail store».

The created document assumes the following set of transactions

The subcontos are filled out and the postings are current. Now a cash receipt order is created

No postings are generated during the document posting process. And the need for a receipt order lies in the need to reflect it in the cash book and print it out.

It is worth noting that in this case it is not necessary to follow the sequence of creating documents, but then you will have to create each of the documents separately.

1C offers ample opportunities for maintaining retail trade records. In this article we will look at:

- how to reflect retail sales in 1C 8.3 Accounting;

- what is important to consider when filling out the document Retail Sales Report in 1C 8.3;

- what determines which transactions will be generated in 1C for retail trade.

In retail trade, outlets are differentiated by automation. Automated and non-automated point of sale in 1C 8.3 - what is it?

- An automated point of sale (ATP) is a retail point where orders are issued during the day. At the end of the shift, the cash register is closed and a detailed report on retail goods sold is generated.

- A non-automated retail outlet (NTP) is a retail outlet in which cash register receipts are not reflected in the database during the day, and only a detailed report on goods sold for a certain period is entered into it.

Setting up retail accounting

If the organization is engaged in retail trade, then in the settings in the section Main - Settings - Accounting Policy set Method for evaluating goods in retail :

- By purchase price- goods in the warehouse are accounted for at cost, while the trade margin on account 42 “Trade margin” is not taken into account. The cost of goods is recorded on the account “Goods in retail trade (at purchase price)”.

- By sales price- goods in the warehouse are accounted for at the selling price, while the trade margin on goods is reflected in account 42 “Trade margin”. Accounting for the cost of goods is carried out:

- for ATT - “Goods in retail trade (in ATT at sales price)”;

- for NTT - “Goods in retail trade (in NTT at sales price).”

If goods are accounted for at sales price, determine for NTT.

Retail outlets (warehouses) in 1C

Retail outlets are reflected in the directory Warehouses In chapter Directories - Products and services - Warehouses.

It is in the warehouse card that it is specified that it is a retail store or a manual point. This sign is indicated in the field Warehouse type :

For NTT, if accounting is carried out in sales prices, also indicate Nomenclature group of retail revenue . Then when holding the document Retail sales report in 1C 8.3, analytics will be filled in for account 92.01.1 “Revenue from activities with the main tax system.”

Be sure to ask Price type for retail (including NTT) warehouses. And also set the price using the document Setting item prices .

Automated point of sale in 1C 8.3

Let's look at how to fill out a report on retail sales in ATT using an example

The organization retails goods through ATT. Accounting is carried out without using account 42 “Trade margin”.

On April 18, the following goods were sold to individuals at total amount 70,800 rub. (incl. VAT 18%):

- Blinds “Plastic (white)” - 20 pcs. at a price of RUB 3,540.

Payment for goods is made in cash at the cash register.

Retail sales of goods

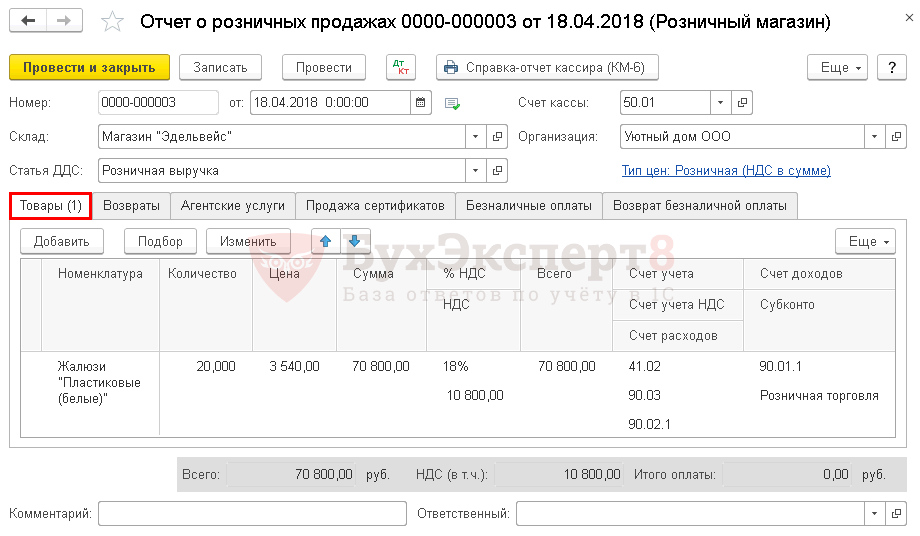

Fill out a detailed report on goods sold in ATT document Retail sales report type of operation Retail store In chapter Sales - Retail Sales - Retail Sales Reports - Report - Retail Store.

- Stock directory Warehouses, Warehouse type Retail store.

On the tab Goods indicate the products sold from reference book Nomenclature.

- Account are filled in the document automatically, depending on the settings in the register Item accounting accounts . If necessary, it can be changed manually. Find out more about.

- Subconto- product group related to retail trade is selected from directory Nomenclature groups.

If payment is not made in cash at the cash desk of a retail store, then indicate all types of non-cash payments (payment card, electronic means, etc.) on the tab Cashless payments .

Postings

Postings in ATT will be standard and depend only on the accounting policy settings (which account is used).

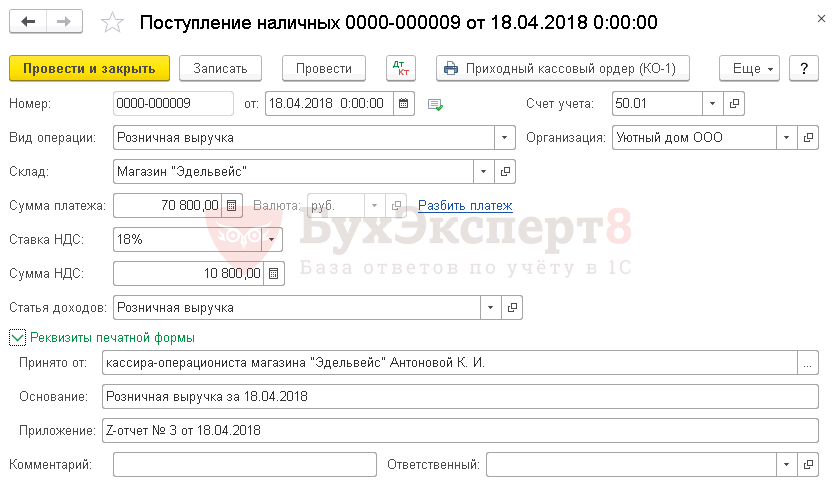

At the end of the shift, when delivering retail proceeds from the operating cash desk to the organization’s main cash register, a cash receipt order is created (clause 4.1 of Bank of Russia Directive No. 3210-U dated March 11, 2014).

based on document Retail sales report by button Create based on – Cash receipt.

In the document please indicate:

- Stock- retail point, selected from directory Warehouses, Warehouse type Retail store;

- Amount of payment

The document does not generate transactions in accounting and accounting records. Cash receipts from the debit of the “Organizational Cash Desk” account are reflected in the document Retail sales report .

Using this document you can create printed form Receipt cash order (KO-1).

Manual point of sale in 1C 8.3

Let's look at how to fill out a report on retail sales in NTT.

The organization retails goods through NTT. Accounting is carried out without using account 42 “Trade margin”.

- Fabric “Blackout Scarlett” - 100 linear meters.

- Fabric "Jacquard Sylvia" - 100 linear meters.

There were no other receipts to the warehouse during May.

In May, retail revenue in the amount of:

- May 06 - 12,980 rub.

- May 18 - 11,210 rub.

- May 23 - 14,750 rub.

- May 31 - 8,850 rub.

- Fabric “Blackout Scarlett” - 65 linear meters.

- Fabric "Jacquard Sylvia" - 20 linear meters.

On the same day, based on the inventory, a retail sales report was generated for a total amount of 47,790 rubles:

- Fabric “Blackout Scarlett” - 35 linear meters. at a price of 826 rubles.

- Fabric "Jacquard Sylvia" - 80 linear meters. at a price of 236 rubles.

Unlike ATT, in this case, the capitalization of retail revenue is first recorded, and then a detailed report on goods sold is entered.

Posting retail revenue to the cash register

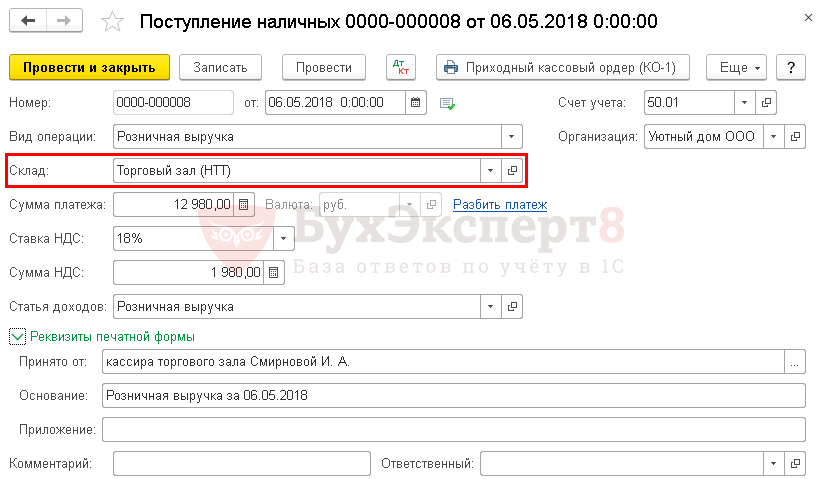

The entry of retail proceeds into the main cash register of the organization is formalized document Cash receipt transaction type Retail revenue In chapter Bank and cash desk - Cash desk - Cash documents.

In the document please indicate:

- Stock- retail outlet, selected from the directory Warehouses , Warehouse type - Manual point of sale;

- Amount of payment - the amount of retail revenue deposited at the cash register.

Postings

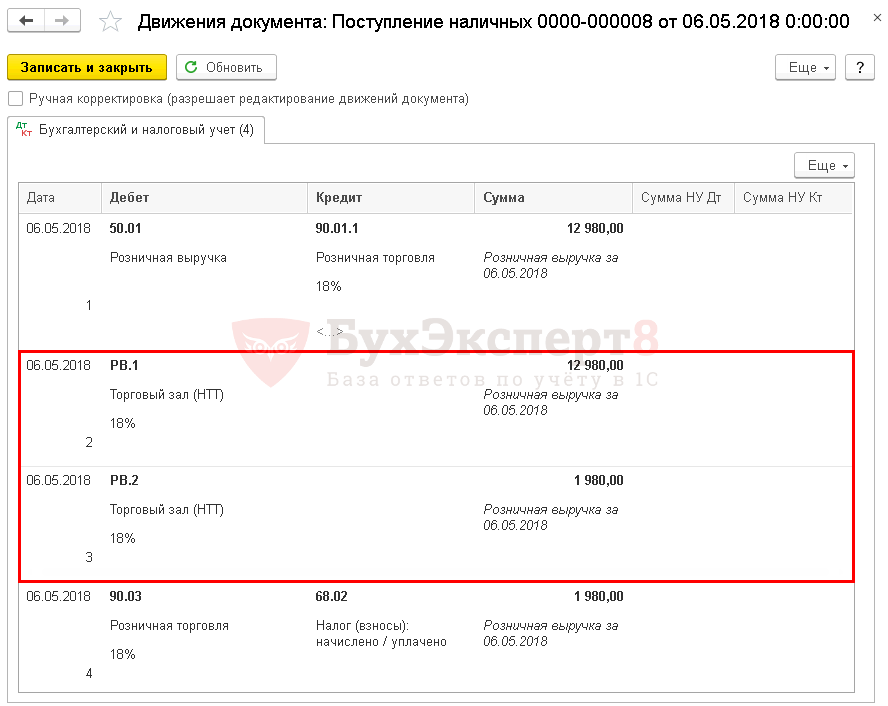

Revenue received at the cash desk from a retail store (NTT) is considered undistributed until the document is entered Retail sales report , and is reflected by:

- Dt - revenue,

- Dt - VAT.

Retail sales of goods

Fill out a detailed report on goods sold in NTT document Retail sales report type of operation Manual retail outlet In chapter Sales - Retail Sales - Retail Sales Reports - Report - Manual Point of Sale.

Receiving cash revenue from retail sales imposes certain responsibilities on the organization. If settlements between organizations for the sale of goods, works, and services occur mainly by non-cash payment, then settlements with individuals usually occur in cash, less often - using electronic means payment.

In this article we will examine in detail the preparation of cash documents, accounting, tax accounting and postings for retail revenue that comes in the form of cash from individuals. Let's touch a little on the need to use cash register equipment.

1. Selling for cash with a cash register

2. How to register retail sales

3. How to fill out the cashier-operator log

4. Retail sales report

5. PKO for retail revenue

6. Entering PKO data into the cash book

7. Postings for retail revenue - example

8. Retail invoice and sales ledger

9. Retail accounting using the simplified tax system

10. Report on retail sales in 1C: Accounting

So, let's go in order. If you don't have time to read a long article, watch the short video below, from which you will learn all the most important things about the topic of the article.

(if the video is not clear, there is a gear at the bottom of the video, click it and select 720p Quality)

We will discuss the topic further in the article in more detail than in the video.

1. Selling for cash with a cash register

Entity or an individual entrepreneur planning to accept cash as payment for his goods, work or services or make payments using payment cards, first of all decides whether he is obliged to use cash register equipment, or whether other forms of confirmation of payment acceptance can be used.

The scope of application of cash register equipment (CCT) is regulated by the federal law dated May 22, 2003 N 54-FZ “On the use of cash register equipment when making cash payments and (or) payments using electronic means of payment.” In 2016, global changes were made to it.

Despite the fact that the topic of this article is not directly devoted to the use of cash registers in calculations, we will touch upon this issue. Because Further paperwork directly depends on this.

CCP is used by all organizations and individual entrepreneurs when they make cash payments or payments using payment cards in the case of the sale of goods, performance of work or provision of services. This is the default condition.

Terms of mandatory use of CCP when paying cash and cards with customers:

- - from February 1, 2017 - for those who are already using CCP

- - from July 1, 2018 - for organizations and individual entrepreneurs providing services to the population (now they issue BSO), for taxpayers on UTII and patent (now they can issue sales receipts at the request of the buyer), owners of vending machines.

Cash registers used in calculations must allow online transmission of calculation data to the tax office via the Internet. fiscal data operator(OFD). The buyer can receive either a paper check or a check email(this will be implemented through a special application on buyers’ phones).

There are a number of exceptions when CCP may not be used. Among them, for example, the sale of newspapers and magazines, travel documents, trade at markets and fairs, peddling trade, sale of kvass and milk from tanks, hawking vegetables, etc. Also, cash register systems are not used for settlements in remote and hard-to-reach areas.

Therefore, in the near future, when selling for cash, it will be mandatory to use a cash register, with very limited exceptions.

2. How to register retail sales

So, from now on we will assume that you are using a cash register. But simply running a check on a cash register and handing it over to the buyer (send it to him by email) is not all. Or rather, everything is just beginning, since you need to know how to document retail sales.

You should clearly understand the differences between the operating cash desk and the main cash desk of the organization. Operating cash– this is a box with cash at the cash register (the accounting document here is the cashier-operator’s journal). Main (main) cash desk- this is the money for which the cash register limit is established (the accounting document is already different - the cash book).

First, we will discuss the responsibilities of the cashier-operator for accepting funds and processing documents. Then we will analyze the procedure for transferring cash from the operating cash desk to the main one.

So, during the sale, each buyer is punched and given cash receipt. All movements on the operating cash desk are reflected in Cashier-operator's journal. In connection with the transition to online cash registers, it is not yet clear whether this journal will need to be maintained in the future or not. But while it is in use, it has not been cancelled, so we will discuss the procedure for maintaining and filling it out.

Regulations:

- “Standard rules for the operation of cash registers when making cash settlements with the population” (approved by the Ministry of Finance of the Russian Federation on August 30, 1993 No. 104, applied to the extent that does not contradict Law No. 54-FZ)

- "Album unified forms primary accounting documentation for accounting of monetary settlements with the population during the implementation of trading operations using cash registers" (forms approved by Resolution of the State Statistics Committee of the Russian Federation dated December 25, 1998 No. 132) - this document approved the form of the Cashier-Operator Journal KM-4.

Despite the dates, these documents are current.

The cashier-operator's journal is used to record transactions regarding the receipt and expenditure of cash (revenue) for each cash register machine of the organization, and is also a control and registration document of meter readings. The cashier-operator's journal KM-4 is the main document reflecting the movement of cash in the store's cash register. It is set up for each cash register separately.

3. How to fill out the cashier-operator log

The journal must be laced, numbered and sealed with the signatures of the head and chief accountant of the organization.

All entries in the “Journal of the cashier-operator” KM-4 are kept by the cashier-operator in chronological order, line by line, without spaces, in ink or a ballpoint pen.

Entries are made on the basis z-reports(report with cancellation), which are taken at the end of the working day (shift). We will not give examples of z-reports, because... their appearance depends on the cash register used.

Each new report must be formatted on a new line. You can see an example of filling in the screenshots below.

If three shifts and different cashiers work on one cash register, then three separate lines from the same date must be entered.

Pay attention to column 11 “Deposited in cash” - this column indicates only the amount of cash received from customers (card payments and returns are not included).

An entry in the journal should be made every time a shift at the cash register was opened, even if no cash was received at the cash register for the day.

4. Retail sales report

After the z-report is taken and the next line in the cashier-operator’s journal is filled in, certificate-report of the cashier-operator according to form No. KM-6. The certificate report reflects the readings of the cash register counters at the beginning and end of the shift, revenue for the day (shift), and the amount returned by customers. These data are identical to those entered in the cashier-operator’s journal.

The Z-report is attached to the cashier-operator’s certificate (retail sales report) and, together with cash proceeds, is submitted to the main cash register.

5. PKO for retail revenue

So, we found out that at the end of the working day, retail revenue is transferred from the operating cash desk to the main cash register. In this case, the cashier of the main cash register receives (from the cashier or senior cashier) cash proceeds, a certificate from the cashier-operator (retail sales report) and a z-report attached to it.

The cashier must issue a PKO in the name of the person depositing cash proceeds to the main cash desk (cashier, senior cashier) - for the entire amount of proceeds received from him. If several cashiers hand over the proceeds, then the PCO is issued for each one.

In the line “Accepted from” the full name of the person who is donating the proceeds is indicated, in the line “Base” - retail proceeds (you can also indicate the name of the store or the number of the operating cash register).

The receipt from the PKO is stamped and given to the depositor (cashier).

Data on receipt of cash proceeds is entered into the cash book.

6. Entering PKO data into the cash book

A cash book is a special form (journal) for recording cash transactions, which contains information on all receipts and withdrawals of cash at the organization’s cash desk.

Maintaining a cash book is based on the following: regulations :

- — Resolution of the State Statistics Committee of the Russian Federation dated August 18, 1998 No. 88 “On approval of unified forms of primary accounting documentation for recording cash transactions and recording inventory results”

- — Directive of the Central Bank of the Russian Federation dated March 11, 2014 No. 3210-U.

The first one shows standard form cash book (No. KO-4), the second contains some rules for filling out. A legal entity carrying out transactions with cash, regardless of the taxation system applied, is required to maintain a cash book (clause 1, clause 4.6, clause 4 of Directive N 3210-U). Individual entrepreneurs may not keep a cash book.

You can keep a cash book on paper or in in electronic format :

- - on paper, the book is drawn up by hand or using a computer (other equipment) and signed with handwritten signatures.

- — in electronic form, the book is prepared using a computer (other equipment) ensuring its protection from unauthorized access and signed with electronic signatures.

There are two ways to maintain a cash book on paper:

- — filled out by hand (the book is printed in advance or purchased, bound and pages numbered);

- - filled out using software and hardware (the book is filled out on a computer and then printed).

It is convenient to fill out the cash book using technical means, for example, in an accounting program. Typically, the program generates a cash book automatically, based on the entered incoming and outgoing cash orders.

At the end of each working day, the cashier prints out and signs a sheet of the cash book, and hands over the PKO and RKO issued for the day to the accountant. If no cash transactions were carried out during a working day, no entries are made in the cash book for that day.

During the calendar year (or other period determined by the organization), printed sheets of the cash book are numbered (usually numbering occurs automatically when printed from accounting program), collected in a folder, and at least once a year stitched into a single book, sealed in the same way as a cash book filled out by hand, certified by the signatures of the chief accountant and the head of the organization and the seal of the organization (if you use one).

See below for an example of filling out a cash book.

7. Postings for retail revenue - example

Now that we have dealt with the preparation of primary documents, let's look at the postings for retail revenue using an example.

Ogorodnik LLC is engaged in the retail sale of vegetables to individuals. On September 14, vegetables worth 22,000 rubles were sold, incl. VAT 10%. Individuals pay in cash in the store. The cost of goods sold was 8,000 rubles. Let's make entries for retail revenue:

Debit 50-2 – Credit 90-1

Debit 90-3 – Credit 68– in the amount of 2000 rubles. – VAT charged

Debit 50-1 – Credit 50-2– in the amount of 22,000 rubles. – cash proceeds are deposited into the main cash register

Debit 90-2 – Credit 41- in the amount of 8,000 rubles. — the cost of goods sold is written off.

You can also use account 62, in which case the transactions for retail revenue will be as follows:

Debit 62-1 – Credit 90-1– in the amount of 22,000 rubles. – revenue is reflected

Debit 50-2 – Credit 62-1- in the amount of 22,000 rubles. – the buyer’s debt is repaid.

The rest is all the same.

A few words about the recognition of income for the purpose of calculating income tax. Income is recognized:

- With the accrual method: on the date of sale of goods, works, services.

- With the cash method: on the day money is received in bank accounts or at the cash desk.

In retail sales, if we do not consider prepayment, the moment of receipt of payment for goods, work, services and the transfer of goods, performance of work, provision of services coincides in time. Therefore, the date of recognition of income in tax accounting under the accrual method and the cash method will coincide.

Income will be recognized on the date of sale of goods, work, or services. Those. in our example, Ogorodnik LLC will reflect the receipt of income on September 14.

8. Retail invoice and sales ledger

If the seller organization is located on OSNO, then it is a VAT payer. Consequently, when selling goods, there is an obligation to charge VAT and issue an invoice. However, a retail buyer who purchases goods for his own consumption does not need an invoice.

For this situation, the Tax Code provides a separate rule. According to clause 7 of Article 168 of the Tax Code, when selling goods for cash by organizations and individual entrepreneurs in retail trade, public catering and when performing work or providing services to the population, it is not necessary to issue invoices. It is enough to issue the buyer a cash receipt or other document in the established form.

But the question arises, if an invoice is not issued for retail sales, what then should be recorded in the sales ledger? The Rules for Maintaining the Sales Book (approved by Government Decree No. 1137 dated December 26, 2011) stipulate that in such a situation, the details of the cash register control tape (z-report) generated per day are registered in the sales book.

When filling out the sales book, you will also be faced with the question of what to indicate in columns 7 and 8. This is the name and TIN/KPP of the buyer, you do not have them. You need to put dashes in these columns. In column 2 “Operation type code” you will indicate code 26. This is the code for VAT evaders, including individuals.

9. Retail accounting using the simplified tax system

In tax accounting using the simplified tax system, the date of recognition of income is the date of receipt of funds from the buyer (cash method). Those. for our example, if Ogorodnik LLC works on the simplified tax system, income will be recognized on the same day - September 14, when the sale took place and the funds arrived at the cash desk.

Postings for retail revenue on the simplified tax system will be similar to the previous example, only postings for VAT calculation will be absent.

Retail tax accounting using the simplified tax system is maintained in the Income and Expense Accounting Book. The basis for making an entry in the book will be a cash receipt order, because it is the primary accounting document confirming the deposit of funds into the cash register.

The entry in the book will be something like this:

PKO No. 54 dated 09.14.16

Received from sales to retail customers

10. Report on retail sales in 1C: Accounting

For those who keep records in the 1C: Accounting program - see how to create a report on retail sales in 1C: Accounting in video format.

What problematic issues did you encounter regarding the accounting and processing of retail revenue? Ask them in the comments!

Postings on retail revenue and preparation of cash documents

The peculiarities of retail sales through a manual point of sale, or NTT (for the types of retail points in 1C, see the article) are that in this case it is not possible to register sales directly in the program. Information about already completed sales is entered into the information base - so-called “posthumous” records are kept.

In “1C: Trade Management 8” (rev. 11.3) there are two options for accounting for sales through NTT - manually and based on inventory results. Now we will consider the first option. The registration of retail sales based on inventory results is described in the article.

In 1C, to reflect the sale of goods from a retail outlet and the receipt of funds at the cash register cash desk, a document called “Retail Sales Report” is used.

Let's open the corresponding document log.

Sales / Retail Sales / Retail Sales Reports

In the “KKM cash register” field, select the autonomous cash register cash register of the non-automated retail outlet from which the sale was made.

Important. Manual creation of the “Retail Sales Report” document is possible only if a cash register with the “Autonomous Cash Register” type is selected in the corresponding journal in the “KKM Cash Register” field.

Let’s create a “Retail Sales Report” by clicking the “Create” button. In the new document, the cash register cash register, as well as the retail store linked to it, are already filled in automatically (the latter cannot be changed).

On the “Products” tab, we will enter sold products by manually adding lines (the “Add” button) or selecting (the “Fill - Select Products” button). Please note that the price of the product is also filled in automatically and cannot be edited (since the price is tied to the store).

In the “Client” column, the program inserted a predefined element from the partner directory – “Retail buyer”; it should not be changed.

In addition to the sale of goods, the document is intended to reflect the receipt of payment for goods sold. If no other payment methods are recorded, the program “considers” that payment was received in cash, and when conducting a “Retail Sales Report”, it registers the receipt of money to the cash register indicated in it.

The “Retail Sales Report” document allows you to register payments with payment cards, gift certificates, bonus points, and reflect accrued bonuses. The corresponding tabs are provided for this. Some of these possibilities will be discussed in subsequent articles.

Let's run the document “Retail Sales Report”. After that, by clicking on the “Document Movements” button, you can see movements by registers - goods in warehouses, free balances, cash in cash register cash registers and others.

Report on cash in the cash register of KKM

After the retail sale is completed, we will verify the availability of money in the cash register cash register using a report.

Sales / Sales reports / Retail sales / Cash in cash registers

We will generate a report on our cash register. Receipt of funds from sales into the cash register is reflected.

Transfer of money from the cash register cash register to the enterprise cash register

Cash received during retail sales and located in the box of an autonomous cash register must be transferred to the cash desk of the enterprise. This operation is formalized in 1C using the document “Cash receipt order”.

Let's open the corresponding magazine.

Treasury / Cash / Receipt cash ordersLet’s create a new document with the type of operation “Receipt from cash register cash register”.

In the created document, on the “Basic” tab, in the “Cashier” field, we indicate the recipient of the money - the company’s cash desk (if the cash desk was indicated in the order journal, then when creating a new order it is filled in automatically). In the “KKM cash desk” field, select the KKM from which the money comes.

The amount must be entered manually.

Important. If the organization is a VAT payer, in the cash receipt order for receipt from the cash register cash register, in addition to the receipt amount, you must manually enter the VAT amount.

Don’t forget to indicate on the “Print” tab the details for printing the receipt order.

After filling out the document, we will process it.

If you now reformat the cash report at the cash register cash register, it will reflect both receipts from sales and the issuance of money from the cash register machine - in the column “Reception of retail revenue”.

Statement of cash

The movement of money from the cash register of the cash register to the cash register of the enterprise can be seen in the report “Statement of cash" Let's open this report.

Treasury / Treasury reports / Statement of cashWe will generate a report on our organization. By default, reports are generated in currency management accounting(in our example – US dollars). The report reflects the movement of cash: receipts and write-offs from the cash register cash register, receipts to the enterprise's cash desk.

3.0" step by step reflect all retail operations. In this material we will look at the receipt of products and their movement to retail, sales in retail warehouses, sales of products at non-automated retail outlets, as well as collection or receipt of proceeds to the cash register.

NTT includes trade objects that do not have the opportunity to supply a personal computer, or with a general information base data to establish a connection. This, for example, could be outbound trade or a stall.

Receipt of products to the enterprise

In almost all cases, in order to get into the NTT warehouse or retail warehouse, the products first arrive at the wholesale warehouse. It is then processed in this warehouse and moved to retail.

We will not describe the arrival at the wholesale warehouse, since we have dedicated a separate material to this. Just to make our further actions clear, we will give an example of filling out a 1C document:

in the 1C program for retail

After entering 1C, it is necessary to set retail prices for products. To carry out this operation, use a document called “Setting item prices.” The latter is entered in the section named “Warehouse”. But we will generate a document based on the receipt document. First, you need to go to the previously generated product receipt document and press the button called “Create based on.” Once done, select the item named “Set item prices” in the drop-down list.

Next, a new document window should open, in which all the basic details will already be filled in. You will only need to specify the price type. Create two such documents at once so that you don’t have to return to this section later. In the existing documents, assign prices of types under the names “Retail price” and “”. The prices must be the same. Further, for example, we offer the document:

The key called “Change” will also provide access to special options for manipulating prices. For example, it is possible to decrease or increase by a certain percentage.

Moving products from wholesale to retail warehouse

And now the necessary products can already be moved from the wholesale warehouse to retail. To this end, in software product There is a document called "Movement of Goods" which is located in a section named "Warehouses".

Before making the move, you need to create two trains - one with the “Manual retail outlet” attribute, and the second with the “Retail” train type.

For this purpose, compositions are formed in the section called “Directories” - “Warehouses”.

We will give the name “Store No. 2” to the first of the compositions, its type is “Retail Store”. We select the price type from the directory with the name “Item Price Types”:

The second one will be called " Shopping room" The warehouse type will be “Manual retail outlet”, the price type will be “Retail”, and the product group will be “Products”.

In addition, we will create two documents “1C 8.3”: moving to the warehouse premises “Trading Hall” and “Store No. 2”. Documents also need to be generated based on the goods receipt document. In this case, all that remains is to fill in the details called “Recipient warehouse” and the quantity of products:

At the end, the products will be in retail warehouses. There is an opportunity to begin processing the sale of prepared products.

"1C": report for a store on retail sales

In order to reflect the sale of products in retail, a document called “Retail Sales Report” from the section named “Sales” will be useful. First, let's prepare a sales document from a retail warehouse. The latter, by the way, is not much different from the document called “Implementation (acts, invoices).” The only difference is that the counterparty is not indicated, and it is immediately possible to reflect the proceeds from the sale itself.

To do this, select a cash register account. For analytics in 1C, you can also fill in the “DDS Movement” attribute. It will be on the cash register account. Example document:

Selling goods in NTT

In the case of sales of products in a non-automated point of sale at the end of the shift we have no information how many products have been sold. But we know exactly how much was moved from the wholesale warehouse. In order to calculate the quantity products sold, it is necessary to calculate the balance of products in the warehouse and subtract it from the receipt quantity. Let's consider an example: fifty packages of sweets were transferred to NTT, but as a result of the trade, thirty packages remained. According to this, twenty packages were sold.

In order to reflect this calculation in the software product, you need to use a document called “Inventory of goods”, which is located in the section named “Warehouse”.

After that, go to the menu called “Warehouse”, then click on the link called “Product Inventory”. And at the end, click on the “Create” button.

After this, add the item in the table and indicate the actual balance for warehouse. It is possible to use a key such as “Fill”. The deviation from the accounting quantity will be precisely our sales of products:

Once done, navigate through the document and click on the button called “Create Based on”, and then select “Retail Sales Report” from the drop-down list. A new document will be generated reflecting the sale of products in NTT.

Reflection of retail revenue in 1C

For now, we'll just write it down, since the document won't be processed at this time. This means that it is also necessary to reflect the receipts of retail revenue in the section called “Bank and cash desk”. For example, here is the document:

Now you need to post a document named “Retail Sales Report”.