Providing management services to your company. A report that will justify the costs of company management services. Documentation of transfer of authority

Currently, the current legislation of the Russian Federation allows for the possibility of concluding individual entrepreneur agreements on the provision of paid services for the management of the company. Meanwhile, regulatory authorities consider such agreements, as a rule, as an option for tax avoidance. In particular, claims are inevitable if an entrepreneur applies the simplified tax system and pays tax at a rate of 6%. Can they be challenged?

16.07.2018Introductory part.

The question of the legality of transferring the powers of the head of a legal entity to an individual - a manager registered as an individual entrepreneur - currently has no clear solution.

On the one hand, part 3 of Art. 5.27 of the Code of Administrative Offenses of the Russian Federation provides for liability for evasion of registration or improper registration employment contract or the conclusion of a civil contract, whereas in fact there is an employment relationship. A fine for offenses of this kind may be imposed:

- for officials - in the amount of 10,000 to 20,000 rubles;

- for legal entities - from 50,000 to 100,000 rubles.

On the other hand, the current legislation does not directly prohibit the conclusion of an agreement with an entrepreneur on the provision of paid services for the management of the company.

Consequently, formally, the organization has the right to transfer the powers of the executive body to the manager - an individual who has the status of an entrepreneur. The implementation of this right depends on the will of the organization itself. Moreover, such a transfer for an organization in equally both attractive and dangerous from a tax point of view.

What is the tax benefit?

Comparative characteristics of civil law and labor relations in the analyzed situation, for convenience, we present it in a table. Let’s assume that the contract establishes the manager’s remuneration in the amount of 50,000 rubles.

|

Indicators |

Labor relations with an individual |

Civil relations with individual entrepreneurs |

|---|---|---|

|

Subject of the agreement |

Execution by an individual labor function |

Performing individual entrepreneurs of a certain type of service |

|

Validity |

Indefinite or fixed-term (if the employment contract is concluded for a certain period) |

A civil contract is always concluded for a certain period |

|

Responsibilities of a tax agent |

The employer, as a tax agent, is obliged to calculate and withhold personal income tax when paying income to an employee and transfer it to the budget |

The customer does not have the responsibilities of a tax agent, since all taxes on income are paid by the individual entrepreneur himself |

|

Personal income tax - 6,500 rubles. (RUB 50,000 x 13%); insurance premiums(at basic tariffs) - Pension Fund of the Russian Federation (22 %), Social Insurance Fund (2.9 %), Compulsory Medical Insurance (5.1 %) - 15,000 rub. (RUB 50,000 x 30%); insurance premiums for “injury” (for example, for class V professional risk the rate is 0.6%) - 300 rub. (RUB 50,000 x 0.6%) |

USNO - 3,000 rub. (RUB 50,000 x 6%); insurance premiums are paid by the entrepreneur |

|

|

21,800 rub. (6,500 rubles are withheld from the employee’s income) |

3,000 rub. (paid by the entrepreneur himself) |

As we can see, with the second version of the relationship, the organization can significantly save on the payment of fiscal payments. Another undoubted advantage of this option is urgent nature relationship between the parties (which guarantees the absence of problems associated with the reduction or dismissal of an employee).

Meanwhile, tax authorities often consider the transfer of powers to manage an organization to an entrepreneur using the simplified tax system as a tax evasion scheme, the purpose of which is to avoid the responsibilities of a tax agent for personal income tax. At the same time, arbitration practice in such disputes is ambiguous. And given that since 2017, relationships in the field of insurance premiums are regulated by the provisions of Chapter. 34 of the Tax Code of the Russian Federation, it can be assumed that disputes about the legality of transferring powers to manage a company to an entrepreneur using the simplified tax system (due to a reduction in the amount of insurance premiums) will flare up with renewed vigor.

Examples of court decisions.

A striking example of a decision that is positive for the organization is the Resolution of AS PO dated January 22, 2015 No. F06-18785/2013 in case No. A65-8559/2014. The essence controversial situation, which arose in 2011, is as follows.

Based on the results of the inspection of the company, inspectors considered that the transfer of powers of its director to an entrepreneur (one of the company’s participants) on the basis of an agreement paid provision services for managing the current financial and economic activities of the company were carried out for the purpose of evading personal income tax (claim amount - 669 thousand rubles).

However, the courts (all three instances) did not see in the company’s actions a scheme aimed at obtaining unjustified tax benefits. In doing so, they gave the following arguments.

Society in accordance with Art. 42 of Law No. 14-FZ has the right to transfer, under an agreement, the exercise of the powers of its executive body to the manager. Such transfer of powers to the manager is the prerogative of the company, since the solution to this issue is within the competence of general meeting participants of the company or its board of directors (supervisory board), if the latter is provided for by the charter (clause 2, clause 2.1, article 32, clause 4, clause 2, article 33 of Law No. 14-FZ).

The coincidence of the powers of the general director with the powers of the manager is due to their performance of the same functions in managing the company, which directly follows from Art. 40 and 42 of Law No. 14-FZ. This circumstance cannot prove the imaginary nature of the agreement on the transfer of powers of the sole executive body to the manager.

The arbitrators of the AS PO also emphasized that the mere registration of an entrepreneur to enter into a disputed agreement does not indicate the illegality of the actions of the parties to the transaction. In turn, having the status of an entrepreneur entails not only the possibility of applying a 6% tax rate (of course, if the entrepreneur applies the simplified tax system with the object of taxation “income”), but also increased liability for obligations.

The interdependence of the company and the manager (the latter, we recall, was one of its participants), according to the judges of the AS PO, does not clearly indicate that the tax benefit received was unjustified. The latter can only be considered unfounded if interdependence influenced pricing.

Note:

The price of a contract for the provision of paid services includes compensation for the contractor’s costs and the remuneration due to him (Part 2 of Article 709 of the Civil Code of the Russian Federation). Income received from providing paid services, are included in the “simplified” tax base. According to the Ministry of Finance, compensation for the manager’s costs incurred in the exercise of the powers of the sole executive body should be included in the income taken into account when calculating the “simplified” tax (see Letter No. 03-11-11/19830 dated 04/28/2014).

At the same time, different conclusions in a similar situation were made by the judges of the FAS UO in Resolution No. F09-4929/12 dated 06/11/2012 in case No. A50-19343/2011. In this dispute, tax authorities were able to prove that the powers of the sole executive body of the company were transferred to an individual entrepreneur in order to obtain an unjustified tax benefit. The outcome of the dispute was influenced by the following circumstances of the case:

- the registration of the manager as an individual entrepreneur was carried out just a few days before the company made a decision to transfer the powers of the manager to him and was terminated immediately after the termination of the agreement on the provision of paid services for the management of the company;

- the entrepreneur did not show due business activity- all actions related to registration, making changes to the Unified State Register of Individual Entrepreneurs, submission tax returns carried out by the company's lawyer in the absence of payment for services rendered by the entrepreneur;

- the amount of income paid to the manager is as close as possible to the income limit that allows the use of the simplified tax system;

- the entrepreneur had no other clients besides the company;

- the contract for the provision of management services with the individual entrepreneur contained signs of an employment relationship;

- The manager’s work schedule coincided with the work schedule of the company’s employees.

Taking into account these circumstances, the courts came to the conclusion that the agreement on the transfer of powers of the sole executive body to the manager, concluded between the company and the entrepreneur, is a labor agreement and was drawn up in order to obtain an unjustified tax benefit.

What's the result?

So, the conclusion of an agreement on the transfer of powers of the sole executive body of the company to the entrepreneur from the point of view current legislation is not illegal, and the exercise of powers of the sole executive body is an illegal business activity. This agreement by its nature is considered a mixed civil law agreement, since it contains certain elements of agency agreements, trust management property, paid services.

Moreover, from paragraphs. 2 clause 2.1 art. 32 of Law No. 14-FZ it follows that not any citizen can be a manager, but only one who is an individual entrepreneur. After all entrepreneurial activity without the formation of a legal entity, in contrast to work for hire, involves independently organized initiative activity of the subject at his own risk without subordination to the rules labor regulations adopted in a particular organization. In other words, the legislator in the analyzed situation initially intends to establish not labor, but civil law relations.

In this case, the entrepreneur (see Resolution of the Ninth Arbitration Court of Appeal dated June 5, 2017 No. 09AP-19171/2017 in case No. A40-11416/2016):

- is in civil legal relations with the company on the basis of a paid service agreement;

- is referred to as a “manager” and is designated as a “manager” in contracts concluded on behalf of the company with counterparties, financial and service documentation, as well as in business correspondence;

- has the right to receive payment for services rendered by him as the manager of the company;

- acquires rights and obligations to manage the current activities of the company on the basis of Law No. 14-FZ, other legal acts of the Russian Federation and the agreement.

The relationship between the company and the manager, regulated by a contract for the provision of services, is not subject to the labor legislation of the Russian Federation. It follows from Law No. 14-FZ that the action labor legislation applies only to relations between the company and the sole executive body of the company (director, general director) (but not managers) and only to the extent that does not contradict the provisions of the said law.

Let us remind you that distinctive characteristics labor relations are (Articles 15, 16, 56 - 59 of the Labor Code of the Russian Federation):

- hiring an employee to a position provided for in the staffing table or assigning a specific job function to him;

- issuance of an order for his employment indicating the position, salary and other essential working conditions;

- remuneration of the employee at tariff rates or official salary(that is, the process of performing the labor function itself is paid, and not its final result);

- subordination of the employee to internal labor regulations.

In this regard, in the contract with the manager, in our opinion, it is inappropriate to include such elements of the employment contract as the systematic daily performance of a certain type of work by the contractor, fixed wages in the form hourly rates(otherwise, there is a high probability that tax authorities and courts will reclassify a civil contract into an employment contract). Moreover, by virtue of paragraph 5 of Art. 38 of the Tax Code of the Russian Federation, the results of services provided for company management do not have a unit of measurement, quantitative volume and price of a unit of measurement. The manager is given the entire volume (and not part) of the powers of the sole executive body, therefore he is also remunerated for managing all current activities without reference to any specific volume of powers performed.

In the above judicial acts, the claims of the controllers arose only in terms of personal income tax, since from 2010 to 2017, extra-budgetary funds were involved in the administration of insurance premiums. Currently, the corresponding powers have again been transferred to the tax authorities (Chapter 34 of the Tax Code of the Russian Federation). And this circumstance, in our opinion, will only aggravate the situation - now they have an additional incentive to prove that the transfer of powers of the sole executive body of the company to the entrepreneur had no effect business purpose and was pretending. Similar disputes have already arisen before (see, for example, resolutions of the Federal Antimonopoly Service dated 02.14.2013 in case No. A65-15483/2012, FAS UO dated 09.10.2007 No. F09-7158/07-S2 in case No. A71-226/07, in which they talked not only about personal income tax, but also about the unified social tax - the predecessor of the current insurance premiums). Attention should also be paid to the Resolution of the Arbitration Court of the Far Eastern Military District dated November 28, 2017 No. F03-4497/2017 in case No. A73-3767/2017, in which the arbitrators agreed with the arguments of the auditors from the Pension Fund of the Russian Federation that the agreement concluded by the company with the entrepreneur on the simplified tax system on the transfer to him the authority to manage the company was, in fact, an employment contract. Therefore, insurance premiums had to be calculated on the amount of payments. In support of their position, the judges pointed out that the contract did not define the terms for the provision of services characteristic of civil law relations (start date and end date), the possible number of stages, or the result achieved by the contractor upon completion of the provision of services. On the contrary, it spelled out the duties characteristic of the labor function that this entrepreneur performed as the head of this company, and not as a manager.

Managing an organization is continuous operation on a comprehensive impact on the functioning of the organization as a whole, as well as on each of its employees individually to achieve all its goals. The management process involves the use of all possible resources of the organization, as well as full coordination and consistency of management actions to obtain the necessary results of the organization.

Organizational management goals

The goals of managing an organization are to maximize profitability, increase the level of operational efficiency in all areas, solve organizational issues each structural element.

Change management

Crisis management

Our company was founded in 2000 in Yekaterinburg; regional offices were opened in Moscow and St. Petersburg in 2001. Now the company operates in the market of almost all countries of the former CIS, general representative offices are located in Russia, Kazakhstan, Georgia, Belarus, and Ukraine.

The company is one of the leaders in the Russian and Ukrainian consulting and automation markets in the field of strategic, financial and process management, development and implementation of key performance indicators (KPI).

A few words in a sentence that exceed the dimensions of the image. In the following blocks there are types of consulting; by clicking on the “Details” button, we go to a separate page of the corresponding section:

Project management

Our company was founded in 2000 in Yekaterinburg; regional offices were opened in Moscow and St. Petersburg in 2001. Now the company operates in the market of almost all countries of the former CIS, general representative offices are located in Russia, Kazakhstan, Georgia, Belarus, and Ukraine.

The company is one of the leaders in the Russian and Ukrainian consulting and automation markets in the field of strategic, financial and process management, development and implementation of key performance indicators (KPI).

A few words in a sentence that exceed the dimensions of the image. In the following blocks there are types of consulting; by clicking on the “Details” button, we go to a separate page of the corresponding section:

Organization management services

Organization management services involve qualified assistance to management in finding effective and well-founded solutions to management problems that arise at the stage of creation, development or restructuring.

*This offer is not an offer. The price is calculated based on the parameters of a specific task.

Successful companies place great emphasis on management management. Previously it was customary to attract a large number of management specialists to monitor key business processes. Now modern technologies allow you to replace a large staff with a minimum number of subordinates - an organization’s electronic personnel management system, the cost of which is affordable even for a start-up business, helps the manager control all actions and adjust the work of personnel for the greatest efficiency.

Where can I buy software for managing human resources of an organization? The answer is simple: contact the manager of the Simpo-Biz holding - the official gold partner of 1C-Bitrix. You can also order from us:

- creating an online store on a mobile platform for selling goods;

- IT management services;

- web project management;

- other new generation marketing tools.

Why you should optimize your business for Bitrix 1C

The proposed online system combines up-to-date tools for coordinating the work of a resource (online store), a simple and intuitive interface with optimal requirements for the level of PC proficiency. The Bitrix24 platform continuously monitors the most up-to-date information about clients, sales and documentation circulation in the company. Director of the company 24 hours a day anywhere in the world from any mobile device. Organization services electronic system Document management systems are available at affordable prices in our region.

Advantages of working with our team:

- We offer website development for the Bitrix platform with an individual approach to its design;

- our web developer will configure the resource within the agreed time frame;

- received finished project will delight you with ease of managing and editing content;

- You will receive additional 24/7 technical support for your online store from the Bitrix24 system.

The service for managing the sale of goods from a team of our experts will help improve the usability of an online store and increase its popularity and traffic in search engines.

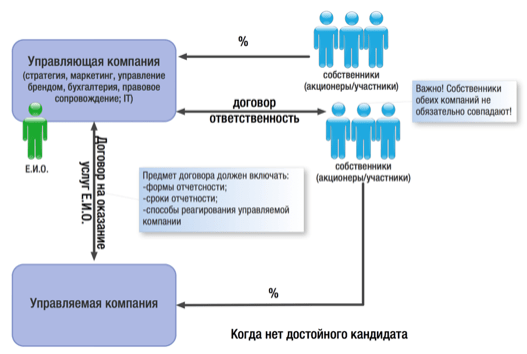

In the course of structuring a business and building a group of companies, the question of maintaining the manageability of the entire group always arises, provided that, as a rule, the management personnel of the business is united and it is impossible to divide it between companies.

As a result, this always leads to the need to search for a management option where the owner remains able to control and influence decision-making both for the entire business as a whole and for any of its segments, despite the economic independence of each group entity.

In this case, when designing a business model, the management company can act as a link between its individual elements.

A management company is any organizational and legal form (in our experience, not only LLC or JSC, but also cooperatives, partnerships, partnerships and even non-profit organizations), which accumulates a complex of strategic, tactical, general marketing (including brand management), organizational, motivational and control functions, as well as functions of scientific and technical development and financial management for all other entities of the Group of Companies.

The formation of such functionality of the management company is due to the following economic and managerial reasons:

1. The need for all entities of the group of companies to have common auxiliary functions:

accounting, legal, marketing and other services, the provision of which by employees of a specialized organization is organizationally and economically more profitable than the creation of similar staff services in each individual company.

Most often, managed legal entities do not have their own lawyer, accountant, or system administrator - all this is handled by the staff of the management company. Objectively, not every business is able to accommodate such a staff in each individual organization of the Group. But even with this option organizational structure there must be a central link that manages local employees.

Therefore, there are cases of creating functionally similar services both in the management company and in the managed society (for example, when the structure is branched, when individual societies are significantly removed from each other and from the management company itself), however, in this case, the management company is engaged in solving strategic problems, then how employees of a managed company perform routine work that does not require highly qualified and knowledge of the strategic plan for business development as a whole.

2. The ability to quickly implement and develop, as well as adjust the previously developed strategy for the group of companies as a whole.

Undoubtedly, business owners need to have complete information regarding its functioning, financial performance, and the degree of effectiveness of previously made management decisions.

In this sense, the value of direct receipt of information about all significant events directly to “headquarters” is invaluable for both owners and top management.

3. Transfer of management from the plane of “he is the most important here, everyone knows him” to the legal field, formalization of relations between the management and subordinate companies through civil legal means and thereby ensuring the necessary degree of control over the activities of managed companies.

In our practice, we have more than once encountered situations where, as a business grows with a small number of owners, new companies are registered, the leaders of which are only formally such; in fact, management is concentrated in the hands of the real beneficiaries.

But there comes a time when the number of personnel and the number of individual organizations within one business reaches a critical level, the owners are not recognized by sight and do not obey their oral orders (and they do not have the right to issue written ones). Even worse, the nominee director can “get things wrong”, because legally he has the right to make decisions, which will lead to unfavorable consequences (primarily of a financial nature).

We must not forget about the costs of paying the nominal manager, which you will incur one way or another, as well as the need to pay social taxes.

Management through the management company helps to avoid such negative aspects.

4. Opportunity legal reduction tax burden through the application of the Criminal Code of the simplified taxation system.

Contractual regulation of the relationship between management companies and managed companies can be mediated by two types of agreements:

contract for the provision of management services;

agreement to perform the functions of the sole executive body.

The choice of one or another contractual instrument depends on a number of factors and the specific structure of the group of companies. Let us consider the features of the application of each of the agreements separately:

Agreement for the provision of management services.

When concluding this agreement, all or some strategic, as well as auxiliary functions in relation to the operational core are transferred to the management company: legal, accounting and personnel support, security, etc., the need for which is felt by all entities of the holding, but the creation of similar divisions in each of them is unprofitable and impractical.

The task of the management company in this case is to determine the main vectors of activity (to develop marketing strategy, carry out scientific and technical development, issue a program of activities for a group of companies for the year, etc.), which must be followed by all managed companies without exception.

It should be noted that the managed company has its own sole executive body (director, individual entrepreneur or other Management company, but in the role of the sole executive body (SEO)), which exercises operational management of the company, makes all current decisions and is responsible for financial result. It is he who is listed in the Unified State Register of Legal Entities as a subject who has the right to act on behalf of the company without a power of attorney.

With such interaction between the individual executive and the management company, the first is limited only by the strategic framework set by the management company, and is completely independent in the process of managing the current activities of his company. Moreover, these frameworks (in the form of reporting forms and periods, as well as a mechanism of responsibility) can and should be laid down both in the agreement with the management company (this is the condition under which the management company undertakes management) and in the agreement with the individual executive organization itself.

However, our experience shows that owners (especially when transforming a single company into a holding) avoid delegating powers to hired managers in every possible way, fearing that they will get out of control.

In this case, reason comes into conflict with feelings: on the one hand, the owner understands the objective need to “give up” the reins of government (a non-core activity specifically for him, employment in another project, the inability to cover all areas of his business), and on the other hand, psychologically cannot come to terms with the fact that his brainchild will be managed by someone else.

In this regard, the issue of trust in the hired manager on the part of the owner becomes particularly relevant.

At the same time, one cannot fail to note the significantly higher degree of personal interest of the director in the results of the activities of the managed company, compared to the agreement on the transfer of functions of the sole executive body, which is automatically reflected in the level of his personal (and not imposed from outside) responsibility.

It is thanks to this instrument of controlled increase in the degree of independence that a synergistic effect from business structuring is achieved - tax optimization can be enhanced by increasing managerial efficiency.

In addition, in the event of any adverse consequences of the activities of the managed company (the simplest example is tax claims), it is unlikely that anyone will be able to definitely assert (and prove) that such consequences occurred as a result of the execution by the director of the managed company of direct orders of the management company.

In other words, the management company will protect itself from negative consequences, and will also have the opportunity to save business reputation and an established image, citing the “amateur activity” of the hired director.

Agreement to perform the functions of the sole executive body

Let us recall that the possibility of transferring authority to manage an organization Management company provided for by a number of federal laws:

For example:

clause 1, art. 42 of the Federal Law on LLC: The company has the right to transfer, under an agreement, the exercise of the powers of its sole executive body to the manager. clause 1 art. 69 Federal Law on JSC: By decision of the general meeting of shareholders, the powers of the sole executive body of the company can be transferred under an agreement commercial organization (management organization) or an individual entrepreneur (manager).

In this case, an agreement is concluded with the management company to transfer the functions of the sole executive body. It is the management company (represented by its director) that receives the authority to act without a power of attorney on behalf of the managed company: to represent the interests of the managed company in all organizations and institutions, as well as to enter into any economic relations. Key managers of the business, its owners in this case are employees and/or participants of the management company and already at its level and on behalf of the management company perform all management functions.

Of course, the director of the management company cannot effectively manage the management company itself, and even all the managed companies, therefore, on the basis of a power of attorney, he delegates his powers to a special employee who will be the actual head of the managed company.

Moreover, such an actual manager is on the staff of the management company (!) and receives a salary from it.

The degree of control of the owners, reporting and responsibility, as well as the degree of independence of the actual manager when making decisions in this case is determined by the provisions of the employment contract with the management company.

A negative consequence of the appointment of such a manager may be a low degree of responsibility and a lack of deep personal interest in the results of the activities of the managed company.

As we can see, there is no doubt that the inclusion of a Management Company in the business model helps solve many difficulties in the presence of an extensive legal structure of the business.

At the same time, taking into account the realities and trends of tax administration, One cannot ignore the question of how the management company is viewed from this side.

After all, the existence of a management company gives grounds to talk about the affiliation of the entities managed by it among themselves (even if the owners of the companies do not coincide). Of course, when we're talking about about, for example, purely accounting and legal services(not about the status of the management company as a single individual organization) and such services are provided not only to organizations connected by contractual relations, but also to outside entities, it will be difficult to recognize affiliation on this basis. In the case of fulfilling the role of the sole executive body, the presence of a single managing entity for several legal entities, which are all the more bound by other agreements with each other (which usually happens if a business is built within a group of companies), will link all organizations into a single structure.

This is not critical if all entities apply the simplified tax system and there is no possibility for the tax savings described above by applying the same criminal code of the simplified tax system. However, such affiliation will attract attention if we are talking about the interaction of entities in different special regimes, which naturally leads to minimizing taxation on business income.

Considering that tax authorities are paying increasingly close attention to such structures, trying to justify the artificiality of their division into several entities or the unreasonableness of the costs of attracting the management company itself, In terms of separating the management company, the following rules must be observed:

1) The types of services provided must be specified. The more detailed the subject of the management company’s activities is described, the more difficult it is to prove the artificiality of its separation in a group of companies (see, for example, Resolution of the Seventeenth Arbitration Court of Appeal dated October 30, 2012 No. 17AP-11284/12: the taxpayer managed to win the dispute by maximizing the detail of evidence of the execution of the contract In the report on the execution of powers of the individual executive officer, the volume of work performed to manage current activities is indicated with a breakdown of the work performed by employees of specific departments (services), and even the volume of hours spent on each service is indicated).

Considering that many companies currently use various software systems, allowing you to track the time spent performing certain tasks by employees, the solution to the task of collecting such information can be automated.

At the same time, the management company, in the role of the sole executive body, carries out the current management of the company, a full detailed description of which is impossible in the contract. Both corporate legislation and, as a rule, company charters usually reserve residual competence for the individual executive officer: “and other things not included in the powers of other bodies of the Company.” Therefore, if the management agreement with the management company in the role of sole executive officer does not contain a specific list of the management company’s powers, it is impossible to talk about the lack of detail in the functions of the management company, and, consequently, its artificial separation. This conclusion is also supported judicial practice:

Due to the very nature of current management activities, it is impossible to comprehensively determine the competence and scope of responsibilities of the EIO (Management Company) not only at the level of law, but also at the level of the company’s Charter, agreement on the transfer of powers, local regulations, since it is impossible to provide for all issues on a daily basis arising in the activities of the managed organization and which are not within the exclusive competence of the general meeting and the board of directors.

Resolution of the Federal Arbitration Court of the West Siberian District of May 12, 2014 No. F04-2761/14 in case No. A81-2271/2013

2) Care must be taken in the description of the procedure for calculating the management company’s remuneration for its services.

So, if you tie remuneration to the achievement of any indicators (growth in revenue, profit, number of clients, etc.) - it is necessary to confirm each time their achievement or non-achievement, formalize all necessary documentation. Otherwise, the tax authority will challenge payments to the management company (Resolution Arbitration Court North Caucasus District dated July 11, 2016 N F08-3871/16 in case No. A01-1790/2015, Resolution of the Fifteenth Arbitration Court of Appeal dated February 16, 2016 No. 15AP-22105/15).

As a rule, the courts, siding with the tax authority, say that they could not confirm what specific work the management company performed and how the cost of each type of its services was determined. Therefore, a description of the procedure for forming the cost of services provided in the contract itself and a breakdown of the final cost for each period of the management company’s activity - required condition work with the Management Company.

Of course, the reward should include everything running costs Management company for maintaining its activities: office rent, payroll for employees, etc. This amount forms the base remuneration amount. If the management company does not accumulate part of the business’s profits, then the remuneration may provide for a fixed fixed amount covering the expenses of the management company with a possible small increase, for example, no more than once a year (in case of an increase in the payroll or other expenses);

The above calculation of remuneration can be complicated if, for example, the payroll of employees depends on their performance indicators and changes from month to month. For this purpose, companies have developed their own systems for calculating remuneration for each employee, which can also be used as the basis for calculating remuneration for management companies. In this case, it will be necessary to detail each indicator to confirm the validity of the management costs in the declared amount.

Along with covering the basic expenses of the management company, remuneration may also include a variable part depending on financial result activities of the management company: for example, as a percentage of the revenue or profit of the managed company. This can be either a monthly increase to the basic remuneration or an “annual bonus” of the management company based on the results of the financial year. In any case, remuneration in this form must be justified by the mandatory growth in revenue/profit of the managed company and confirmation that such growth is related to the activities of the management company and its employees. Moreover, of course, this part of the remuneration should not lead to the fact that the entire profit operating company flows into the management company, which applies a lower income tax rate.

3) Proof of the effectiveness and reality of the management company’s activities will be indicators of growth in revenue, profit, assets of the managed company, which, in turn, for example, led to an increase in taxes paid to it (this indicator will be especially valuable).

4) Evidence of the independence of the management company as an economic entity will be the implementation management functions for several companies, preferably not related to each other (for one, for example, in the role of sole executive officer, for another, providing only accounting services, etc.).

5) High professionalism of the staff of the management company (in comparison with the managed one), increased requirements for their level of education, work experience, etc. will also allow you to confirm professional competence and independence of the Criminal Code (see, for example, Resolution of the Arbitration Court of the North Caucasus District dated January 26, 2015 No. F08-9808/14 in case NА32-25133/2013).

Taking into account the described nuances, it is necessary to carefully approach the legal recording of the actual activities of the Management Company and the procedure for its interaction with its customer of services. In addition to the constant, systematic collection of evidence confirming this activity and its usefulness for the managed companies, problems with the tax authority should not arise.

Today, companies have the right to enter into an agreement for the provision of company management services with individual entrepreneurs for a fee. However, despite the legality of such relationships from the point of view of current legislation, regulatory authorities continue to consider such transactions as a method of tax evasion. It will definitely not be possible to avoid claims from the tax office if the individual entrepreneur uses the simplified taxation system (USNO) “Income” (6%). In this article we will try to figure out whether it is possible to challenge the department’s claims.

Is it possible to conclude an agreement for the provision of company management services with an individual entrepreneur?

There is currently no clear solution to the issue of the legality of concluding an agreement on transferring the powers of a company manager to an individual registered as an individual entrepreneur. Formally, an enterprise has the right to appoint an individual entrepreneur as manager under a contract, although such a decision is dangerous from the point of view of paying taxes.

A direct ban on signing an agreement with an entrepreneur on the provision of services for managing a legal entity for a fee current laws do not contain. But, on the other hand, part 3 of Article 5.27 of the Code of Administrative Offenses of the Russian Federation provides for liability for evasion of registration (improper execution) of an employment contract (conclusion of a civil law contract) at a time when there is actually an employment relationship:

- a fine of 10 to 20 thousand rubles for officials;

- from 50 to 100 thousand rubles fine for legal entities.

Agreement for the provision of company management services with an individual entrepreneur - what is the tax benefit?

To understand what the tax benefit is when concluding an enterprise management agreement with an individual entrepreneur, let us present and analyze comparative characteristics labor and civil law relations (let’s take the fee for performing management functions equal to 100 thousand rubles):

| Indicators | Relations under a civil law contract with an individual entrepreneur | Labor relations with an individual |

| Subject of the agreement | Provision of services by an entrepreneur (for example, company management) | Performance by an individual (employee) of specified labor functions |

| Validity | Specific period (specified in the contract) | Determined in time (fixed-term employment contract). Unlimited in time (unlimited contract). |

| Responsibilities of a tax agent | Since the income tax is paid by the individual entrepreneur himself, the employing company does not have the duties of a tax agent | The employer calculates and withholds personal income tax from the subordinate’s earnings and transfers the amount to the budget |

| Tax according to the simplified tax system – 6000 rubles. (RUB 100,000 x 6%); Contributions to extra-budgetary funds are paid by individual entrepreneurs. | Personal income tax – 13,000 rubles. (RUB 100,000 x 13%); insurance premiums in Pension Fund– 22,000 rub. (RUB 100,000 x 22%); contributions to the Social Insurance Fund - 2900 rubles. (RUB 100,000 x 2.9%); contributions to compulsory medical insurance – 5100 rubles. (RUB 100,000 x 5.1%); contributions to prof. diseases and industrial injuries(let’s say hazard class V – 0.6%) – 600 rubles. (RUB 100,000 x 0.6%). |

|

| TOTAL | 6,000 rubles (paid by the individual entrepreneur himself) | RUB 30,600 (RUB 13,000 is withheld from the employee’s salary) |

After a simple analysis, we can draw the following conclusions:

- By concluding a civil contract with an individual entrepreneur, the company incurs much less expenses for paying fiscal payments.

- The urgent nature of the relationship between the company and the entrepreneur (the GPC agreement always implies a limited duration of the agreement) guarantees that there are no problems with the dismissal or layoff of a worker.

How to competently conclude an agreement for the provision of company management services with an individual entrepreneur

An agreement with an individual entrepreneur for the provision of management services is by its nature a mixed GPC agreement, because in it you can find signs of contracts for the provision of paid services, trust management of property, and orders. It is permissible to sign an agreement with an individual entrepreneur, the subject of which is the transfer of powers of the manager, because:

- the exercise of powers of the sole executive body is not a prohibited business activity;

- the law does not prohibit legal entities transfer under the contract the powers of the sole executive body of the LLC to an individual entrepreneur;

- pp. 2 clause 2.1 art. 32 of Federal Law No. 14-FZ says that the function of a manager can be performed by an individual entrepreneur, and not any citizen (i.e., the law presupposes the emergence of civil law relations, and not labor relations, since the individual entrepreneur independently organizes economic activity at your own risk without submitting to the existing labor regulations at the enterprises).

Important! To ensure that judges in the event of proceedings with the tax service do not re-qualify the GPC agreement as a labor agreement, the terms of the provision of services, the result, and the possible number of stages of cooperation should be determined by the provisions of the agreement.

What points to pay special attention to (based on judicial practice)

When concluding an agreement for the provision of management services with an entrepreneur, it is important to ensure that the relationship does not have signs of an employment relationship (described in the text of Articles 15, - Labor Code of the Russian Federation):

- It is impossible for a manager to obey the internal labor regulations of the enterprise.

- The work of the manager should not be paid according to the official salary or tariff rates (the result of the work should be paid, and not the process of performing duties).

- An Order for employment in the specified position must not be issued; the size cannot be specified. wages and other working conditions.

- You cannot accept an individual entrepreneur as a manager and assign specific labor functions to him.

In such contractual relations between the company and the individual entrepreneur:

- Acquires rights and responsibilities for managing the current activities of the organization (based on Federal Law No. 14-FZ, agreement and other legal acts).

- Receives the right to monetary compensation for his services.

- Referred to as a “manager”, designated as such in business correspondence, contracts concluded on behalf of the organization with counterparties, as well as in official and financial documentation.

- Is in a civil law relationship with the LLC on the basis of an agreement on the provision of paid services.